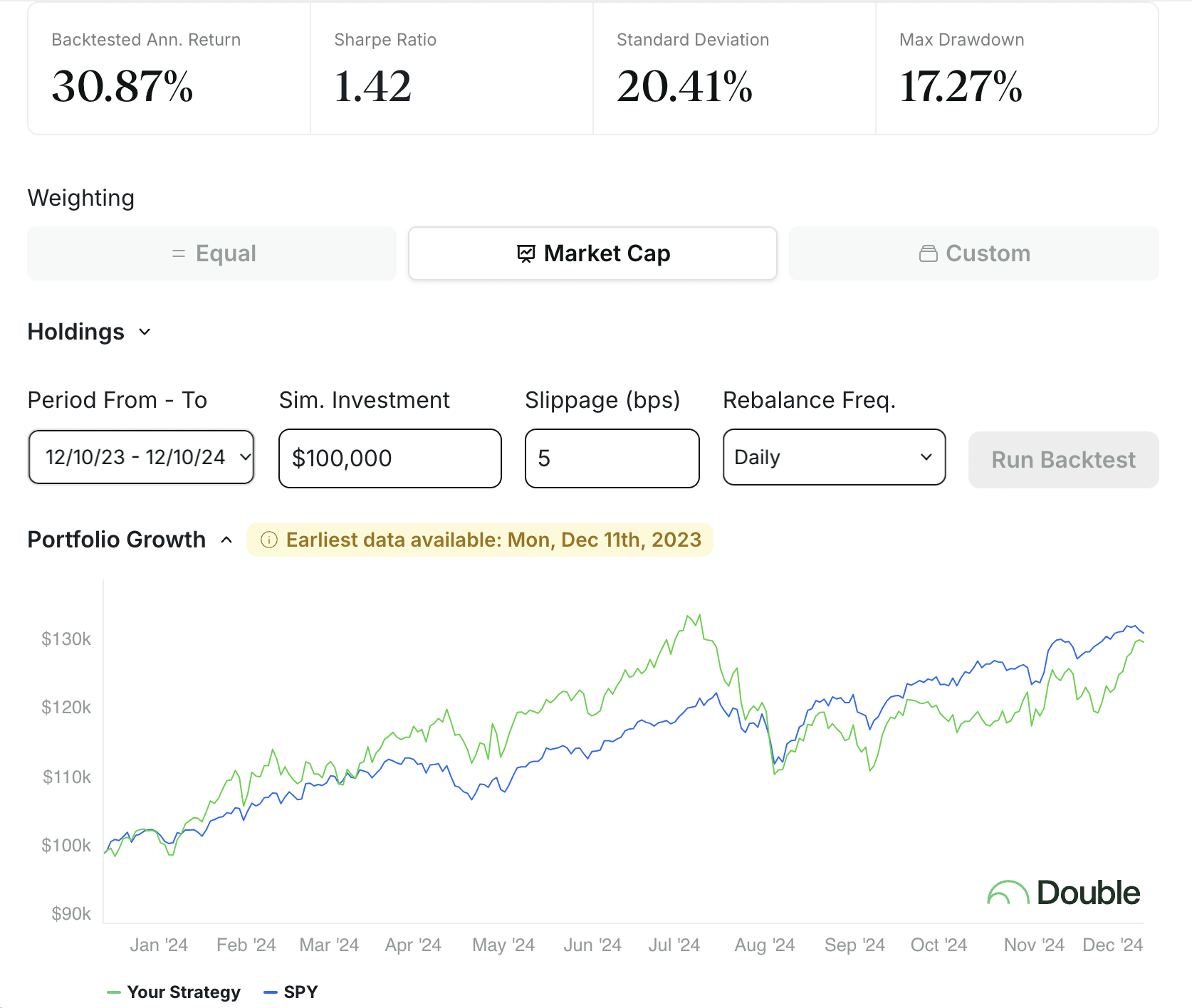

I plugged the stocks mentioned in here into Double's backtesting tool. I couldn't get 6 of the stocks (Samsung, one of the solar ones, 4 other random ones). At least in 2024 the companies listed weighted by market cap produced a return of about 36%, being roughly on par with the S&P 500 (which clearly had an amazing year):

Two thins the post made me thing of (but not yet very much about).

- AI (I think at least) can safely be viewed as improving productivity in a lot of things. That where the value comes from but beg the question of just who actually captures the value (who gets the economic rents here). I'm not sure that it all goes to the AI company as opposed to the production company using the AIs.

- Have you seen any ETFs that seem like good match ups with your portfolio views? If not, would defining and establishing one be at least as good of an idea as that of privately positioning your self? (More work of course but might be a more stable investment strategy.)

To play devil's advocate, would you have said the same thing about computers and the internet (improving productivity in a lot of things)? If so, would you expect it to impact GDP? Because it's not clear that it did. https://fred.stlouisfed.org/graph/fredgraph.png?width=880&height=440&id=RTFPNAUSA632NRUG

I don't think one can easily unpack the impact from either computers or internet (which I'm honestly not sure really has significantly increased productivity) impacts on aggregate productivity just by looking and a graph. GDP is nominal prices basically so technology changes that might well increase output or increase output quality while also working to lower or hold prices constant will be masked in simple GDP traces.

I think you'd need to look at some older models, perhaps like Solow's Growth Model, that include a technology term and see how that is moving around. Total productivity seems like it would be driven by labor, capital and technology state. If one assumes human productivity is pretty constant and the installed capital base is likewise pretty set then innovation like computers, internet and AI should show up in the technology component of the model.

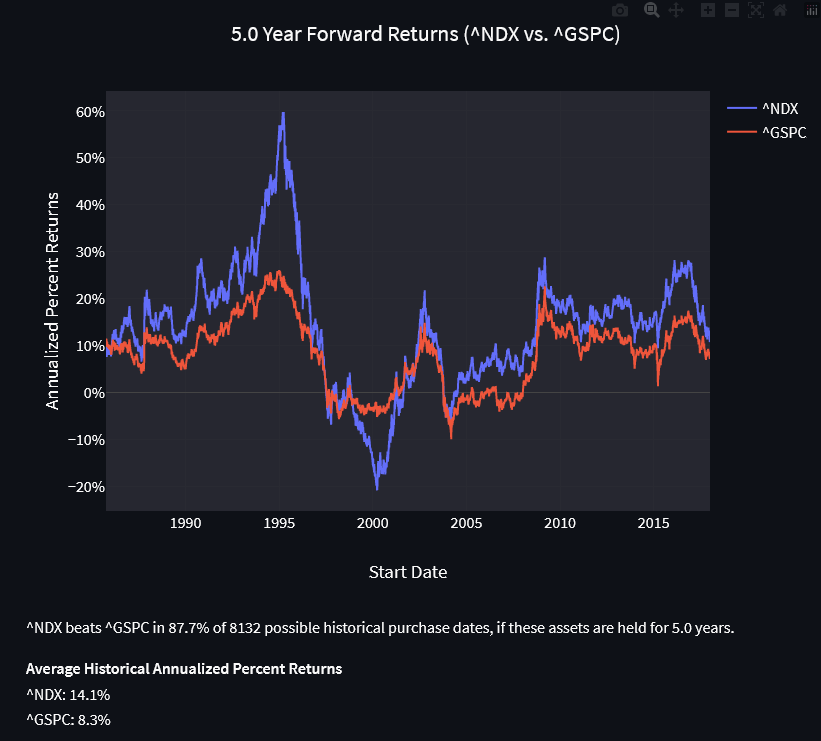

Independent of effects on GDP, the internet (nasdaq100) has still strongly outperformed the overall US stock market (sp500).

I would call it a tie:

- Since 1972, the Nasdaq 100 has experienced slightly higher annual returns (10.8%) than the S&P 500 (10.5%), but it has also experienced much higher volatility.

- During the bull markets, the Nasdaq 100 has crushed the S&P 500 (the 1990s and the post-2008 market).

- However, during bear markets, the S&P 500 has performed much better than the Nasdaq 100 (1973-1974, early 2000s, the 2008 financial crisis).

- The Nasdaq 100 beat the S&P 500 in 25 out of these 46 years (54% of years).

Coincidentally, I made an app to do exactly these types of historical comparisons of returns, with much greater fidelity.

Input ^NDX and ^GSPC (Nasdaq-100 and S&P500 respectively) as the input tickers. These are Yahoo Finance's codes for those respective indices. Alternatively, you can input QQQ and SPY, which are ETFs that track those indices but there will be less historical data since ETFs come after indices.

Nice post. I've been thinking along the same lines and made some investments last year. Perhaps a Discord chat group would be better suited to discuss this, I'd join.

TSMC is a giant when it comes to semiconductors that cannot be ignored, but there are risks related to China-Taiwan tensions. I'm invested, but I also have out-of-money puts for protection.

When it comes to robotics, have you looked at ISRG?

There's a Discord channel called EA/LW Investing with about 150 people. I don't have permissions to generate invite links, but if you DM me your Discord username, I can ask someone to you add if interested.

I have not looked at ISRG for quite a while. I occasionally look at smaller startups doing medical robotics. But the FDA slows down innovation in this area enough that I'm unlikely to invest in this area anytime soon.

I’m surprised you don’t expect any effect on real estate. I would expect it to be greatly affected by such a transformation, although I’m not sure in which direction.

If unemployment skyrockets because AIs can do everything that most humans can and cheaper, then fewer people would have to live in cities, potentially leading to crashing house prices in cities. The same could also happen if working from home becomes the norm due to VR. On the other hand, if human employment stay high, and productivity increases and we still have to be physically at work, then city real estate prices would likely increase with productivity.

Disclaimer: I have almost no track record in active investing, so don’t take anything I say too seriously.

VR will likely shift the locations where housing is demanded. I consider that somewhat separate from the effects of AI. A shift away from the most expensive cities will mildly increase total demand for housing, by making it easier for people to get the kind of housing that they want. I don't know of any publicly traded companies that are focused on housing in expensive cities. Most housing investments are focused on regions where new homes can be built: suburbs and cheap cities that allow new homes.

my current guess is that the superior access to large datasets of big institutions gives them too much of an advantage for me to compete with, and I'm not comfortable with joining one.

Very much a side note, but the way you phrased this suggest that you might have ethical concerns? Is that right? If so, what are they?

No, I don't recall any ethical concerns. Just basic concerns such as the difficulty of finding a boss that I'm comfortable with, having control over my hours, etc.

I like this post a lot, partially because I think it is an underdiscussed area, partially because it expands beyond the obvious semiconductor type companies. One thing I would add, is that with almost no technology advancement, existing and soon to exist LLMs might make investing in social media (and internet adjacent) companies much more volatile. This is because as far as I can see, the bot problem for these companies should only become worse and worse as AI can more perfectly mimic a real user. This could lead to a kind of dead internet scenario where real humans are somewhat drowned out by noise and have grave implications for whatever stocks are involved-who of course depend on ad revenue. The reason I say more volatile is because there is obviously also upside for these same companies to utilise AI themselves further. My views on it are fuzzy though and it could go either way.

AI Therapy isn't the first domino to fall, AI Customer Service is (it's already falling).

95% of customer service humans can be replaced by a combination of Whisper+GPT; they (the humans) are already barely agentic, just following complex scripts. It's likely that the AI customer service will provide a superior experience most of the time (less wait times, better audio quality at a minimum, often more competent and knowledgeable too, plausibly capable of supporting many languages).

Obviously huge cost savings so massive incentive for companies to replace humans (and why it's already started with even weak chatbots).

Investing in it is tricky, same problem you mentioned at the start - picking which horse is going to win this race, most probably either don't exist or aren't publicly tradeable.

Zoom is a potential frontrunner, they acquired Solvvy last year which suggests some strategic awareness of this trend/potential market.

A related thought I’m having: assuming we have a scenario where personal finances still matters, am I better off keeping my real estate loan and my stocks or is it better to sell 3/4 of my stocks to pay off my loan? I’m particularly worried about a scenario where AIs mean that I (and presumably most other people) will be unemployable. My loan is fixed rate.

Stock market feels like one of the last places that modern AI will have a huge impact on (beyond the basics that are already in use). All the breakthroughs seems to be coming in the form of models which are really bad at non-stationarity and extremely high noise. Could be interesting to build a stack of LLMs that ingests 10K's and macro econ data and tries to infer causal models, but I'm skeptical it'll be better than humans at this for a long while. I think you're safe for now :)

I don't look very much at industry-specific ETFs. They're often weighted by market cap, which is generally bad (it tends to weight highly stocks that are in bubbles). Often the larger companies that get included are not at all pure plays on the ETF's theme. For LRNZ's top holdings: SNOW looks like it might be helped by AI, but I don't understand it well enough to bet on that; CRWD looks more likely to be hurt by competition from AI than helped. And with LRNZ, price/sales ratios are quite high.

AI looks likely to cause major changes to society over the next decade.

Financial markets have mostly not reacted to this forecast yet. I expect it will be at least a few months, maybe even years, before markets have a large reaction to AI. I'd much rather buy too early than too late, so I'm trying to reposition my investments this winter to prepare for AI.

This post will focus on scenarios where AI reaches roughly human levels sometime around 2030 to 2035, and has effects that are at most 10 times as dramatic as the industrial revolution. I'm not confident that such scenarios are realistic. I'm only saying that they're plausible enough to affect my investment strategies.

Companies working on AI

Google's DeepMind seems a bit more likely than any other company to produce valuable AI. That's a good enough reason to hold a modest position in Google. TPU and Waymo are additional AI-related reasons for holding Google stock.

OpenAI is a serious contender. Microsoft has a $1 billion stake in OpenAI. But profits from that seem to be capped at 100x, so the best case scenario seems to be that Microsoft shareholders get $13.40 per share from that stake. Maybe Microsoft will invest more in OpenAI. I only see Microsoft getting a modest boost from AI.

Conjecture sounds quite promising. I offered to invest $100k in them this summer. They don't seem interested in investments that small.

There are other new private companies that I haven't been able to evaluate. Here are some that seem worth paying some attention to:

That's a dramatic pace of new startups being founded that look potentially important. VC's seem to have been throwing enough money at them in mid-2022 that they likely had little reason to talk to more ordinary investors such as myself. Investment in such startups has maybe cooled slightly now that FTX has stopped throwing money at them, but I'm guessing it hasn't cooled much.

I see a 50% chance that one or more of these new startups will make DeepMind and OpenAI irrelevant. I have little hope of being able to buy a diversified portfolio of such startups, so I don't expect to profit from direct investments in companies working on AI.

Computing Hardware Companies

The most promising investments involve the hardware needed to power AI. That mostly means semiconductors.

Semiconductor capital equipment companies seem more promising than companies that are more directly involved in making chips, as capital equipment is more cyclical, and less dependent on specific uses.

My current semiconductor-related investments are (in alphabetic order): AMKR, AOSL, ASML, ASYS, KLAC, MTRN, LSE:SMSN, TRT.

I'm likely to buy more sometime in 2023, but I'm being patient because we're likely at a poor part of an industry cycle.

Others that I'm considering buying: ACLS, AMAT, INTC, LRCX, MU, and PLAB.

Some of you will be surprised that I didn't suggest NVDA. Its PE and price/sales ratio are high compared to my other semiconductor investments. I can imagine buying it if its stock price drops relative to other semiconductor stocks. But I suspect its fans underestimate the risk of competition from hardware that is optimized more specifically for deep learning.

I've invested in privately held Fathom Radiant, which seems to have a shot at NVIDIA-like success in AI-related hardware. I'm unsure whether they'll want any more investment in 2023.

I've seen some noise about neuromorphic computing. I suspect that such research is far enough from commercialization that it's hard to figure out how to invest in it. (Also, I'm nervous about helping to speed up AI, as it's already coming fast enough to worry me.)

I have a tiny position in Everspin Technologies (MRAM), mainly because of vague suggestions that their technology will support neuromorphic computing. I haven't found much substance to that speculation, so I think of it as a real long-shot. Maybe a 2% chance of a 500x return this decade, without a high risk of the stock becoming worthless?

INTC also does some neuromorphic work, and seems to be a relatively safe investment even if it lags behind the cutting edge.

Datacenters

Datacenters seem likely to become a major industry, but I don't see great investments here.

AMZN, MSFT, and GOOGL are likely to get some benefit from datacenter growth. I guess I'll expand my GOOGL holdings and buy small positions in AMZN and MSFT sometime in 2023, when I see signs that their stock's downward momentum has dissipated.

EQIX is an example of a company whose revenue growth seems likely to accelerate. But that will be capital-intensive, causing the company to sell enough shares that revenue per share growth doesn't look very impressive. Also, its PE is high.

AAOI is a floundering company that gets over 30% of its revenues from selling products to datacenters. It might recover and profit from datacenter growth, but I'll wait for its losses to shrink before buying.

Semiconductor stocks seem to be strictly better ways of benefiting from datacenter growth than datacenter-specific stocks.

Robotics

AI seems to be on the verge of turning robotics into a major industry. But it's still hard to see when and where the key advances will happen. I suspect the main winners will be companies that aren't yet public, as I'm not too impressed by the opportunities I see so far. I'm playing this mainly via tiny positions in LIDAR companies (INVZ, OUST, LAZR) and SYM.

I have a moderately large position in OSS, whose ruggedized computing products have some robotruck applications. I should look more carefully for other companies that make robotics-related hardware.

Energy

Electricity use is likely to become a larger fraction of the economy as AI takes off. AI is energy-intensive, and will catalyze much more digital activity.

Utility-scale solar seems likely to supply an important fraction of that additional electricity.

My two biggest solar bets are CSIQ, and SCIA. I have smaller positions in JKS, DQ, SEHK:1799.

For power grid infrastructure and solar farm construction, I have positions in MTZ, MYRG, PLPC, and PRIM.

I consider it somewhat likely that nuclear energy will somehow grow more important as a result of AI, but I'm pretty fuzzy on the details. Fusion is likely to be feasible in the 2030s, but I have little idea as to whether it will be competitive.

For fission, there's SMR, uranium mining companies, and uranium futures. I haven't invested in these, and I'm not in any hurry to decide which of these to buy.

Others

Here are some weak guesses about how AI will affect existing companies that make up significant parts of current portfolios, by industry:

We should also think about the effects of an AI-induced general increase in economic growth. Some of the biggest winners in that scenario will be commodified industries where capacity is slowest to change: oil and gas, mining, and shipping.

Other scattered thoughts

I see many changes coming that are hard for investors to exploit.

For example, many forms of therapy seem ripe for being replaced by AI. Most patients can't find top-notch therapists. Therapists have little ability to document their successes. Even when they are able to get a reputation as a great therapist, they can't scale up to serve more than a tiny fraction of the clients that need them.

AI can eliminate the latter problem. The reputation problem is much harder. If one out of every 10,000 patients publishes informative reviews of the AI, that will generate reputations that are much more informative than those of current therapists (assuming that fewer reviewers are actively creating noise).

If the system gets good enough feedback about the results of its advice, it will only take a few years to accumulate better knowledge than the top 1% of therapists. I imagine an AI therapist who has treated a few million patients will be able to usefully sort patients into thousands of categories, and, for the average category, the AI will have tried a dozen different approaches, and will remember which ones worked best. The AI doesn't need an IQ of 100 to translate that specialized knowledge into a large advantage.

Some countries will adopt enough regulations that prevent AI therapy. Will they be able to prevent patients from learning about and finding ways to use AI therapists that are launched in other countries? I'm mildly optimistic, but not willing to bet much.

That might cause an important decrease in prescription drugs for mental health. It seems premature to short the relevant stocks, but I'm going to start paying attention to that area (see the new etf SANE).

I expect that in something like 5 years, several AIs will be created that are able, given enough capital, to make stock markets too efficient for me to be able to measurably outperform the market. Should I prepare to retire from this career? The "given enough capital" part won't happen instantly. There's lots of investment funds that will be slow to adopt AIs, and there are a moderate number of market inefficiencies that will remain until a lot of capital is mobilized to eliminate them. So I'm unlikely to retire as a stock market speculator before 2030.

Can I be one of the leaders in applying AI to the stock market? I plan to think more about this, but my current guess is that the superior access to large datasets of big institutions gives them too much of an advantage for me to compete with, and I'm not comfortable with joining one.