I feel like this underestimates the difference between what you're citing, valuation growth over 2 years post-YC, and the Garry Tan quote, which was about weekly growth during the 3 month YC program. I also wish the original Garry Tan claim were more specific about the metric being used for that weekly growth statistic. In principle, these aren't necessarily mutually exclusive claims. In practice, I'd expect there's some fudging going on.

I can imagine something like the following: Companies grow faster with less investment, reaching more revenue sooner because of GenAI. But, this also means the company has fewer defensible assets, and less of a lead over competitors, so the valuation is lower after 2 years. AKA potentially the cost of software innovation is going down, speed is going up, and there's less of an advantage to being first because it's getting easier to be a fast follower. In a world where it's possible-in-principle to think about one person unicorns, then why should software companies ever have high valuations at all, once enough people know what they're trying to build?

I'm curious what effects with would have, if true. If we end up in a place where an individual can build a $10-20M company, practically on their own, in months, with only a seed round, but can never get to $100M or $1B, how does this affect startup funding models? Pace of overall innovation? I could see this going really well (serial founders have time in their careers to build 50 companies, cost to access new software products drops) or really badly (VCs lose interest in software startups, innovation slows to a crawl), or any number of other ways.

Or, also not mutually exclusive with the above: Maybe GenAI-2023 is sufficiently different from GenAI-2025 that we shouldn't really be comparing them, and the 2023 batches were growing less or slower due to dealing with the aftereffects of covid or something.

The difference between GenAI-2025 and GenAI-2023 in terms of their ability to assist software engineering efforts is quite drastic indeed.

Yeah, my guess is that what Garry was saying is technically true but does not actually imply that companies are growing quickly in a more meaningful sense. Would love to learn more if someone has access to that data.

Disclaimer: I'm an AI YC founder from a recent batch (S24). I have no access to internal metrics about YC's portfolio, but I keep in touch with some startup founders from my batch, and we trade insights and metrics.

Anecdotally, my sense is that YC has done a particularly poor job of evaluating AI startups. Mostly this comes as a result of not taking AGI seriously, and YC's general philosophy of picking companies with impressive founders rather than evaluating ideas directly. YC has essentially bet as if AGI is a platform like smartphones and model quality is not going to improve, which at least for the last two years has been very wrong.

There are basically two ways to add value as an "AI wrapper" company. You can either:

- Try to build scaffolding around AI models so that they're capable of accomplishing some long horizon task they're not currently able to accomplish end-to-end.

- Build an alternative interface that is more useful for a given task than the general chat interface.

Companies in the #1 bucket are the quintessential YC startup of the last few years, something like "An AI that can do your accounting". The way most of them tackle the problem is by breaking it down into pieces and doing context engineering. Investors love these startups because their potential TAM is huge ("all of accounting!"), they sound like they provide the possibility of deep technical moats, and the utility of the imagined solution is really obvious.

But if you look at the fastest growing companies of the AI era - Cursor, Lovable, Bolt, Windsurf - the majority of their utility comes from providing an interface for something the LLMs can do on their own. In some cases (Cursor, for instance) these companies started by offering custom flows for tasks and then deprecated them in favor of simple AI agents later.

This is because it's hard to get performance that's much better than what you get natively from the API. In some cases the scaffolding is important, but more typically the models are either so good they can just OODA all by themselves, or else they're not good enough to get a startup to product market fit even with scaffolding. And because these models are improving all the time, even if your wrapper is really effective now, often the models improve quickly enough that all of the hard work you've done becomes moot too quickly to matter.

As we get closer to AGI I expect these dynamics to start reversing the growth even some companies that have done well so far. For example, YC has funded like 5 PR review companies, including Greptile. In 2023, it was really easy to improve base model performance as a PR review company - just ingest the diff, search for related bits to what's being changed, and pull those bits into context. But now it's 2025, and, because PR review is a short-horizon task, it's been one of the first things to fall; you can get better performance by running Claude code with a github action than by using any of these solutions. I don't actually know what these companies are going to do in the future other than hope their customers don't notice.

I'd be very interested in if this is due to the US economy as a whole being worse now than in 2009. Could we compare with growth rate of AI companies in countries with better economies?

and with actual revenue.

“It’s not just the number one or two companies -- the whole batch is growing 10% week on week,”

YC makes all startups in the batch report KPIs even from before being accepted into the batch, If you participate in their Startup School, you are asked to track and report weekly numbers, such as number of users.

Paul Graham posts unlabeled charts from YC startups every now and then, so I assume the aggregate of all of these is what Garry Tan is refering to. Unfortunately, it is not possible to reproduce his analysis. But we should see the effect with the next round of exits. They should happen faster or at higher valuations compared to previous batches.

It seems safe to assume that most YC companies were not using it much before the launch of ChatGPT (if only because the technology wasn’t available)

Strictly speaking the technology was available (I got a startup that I consulted for to adopt GPT-3 roughly a year before ChatGPT happened). That said, it wasn't very widely known, so your take still seems like a reasonable approximation.

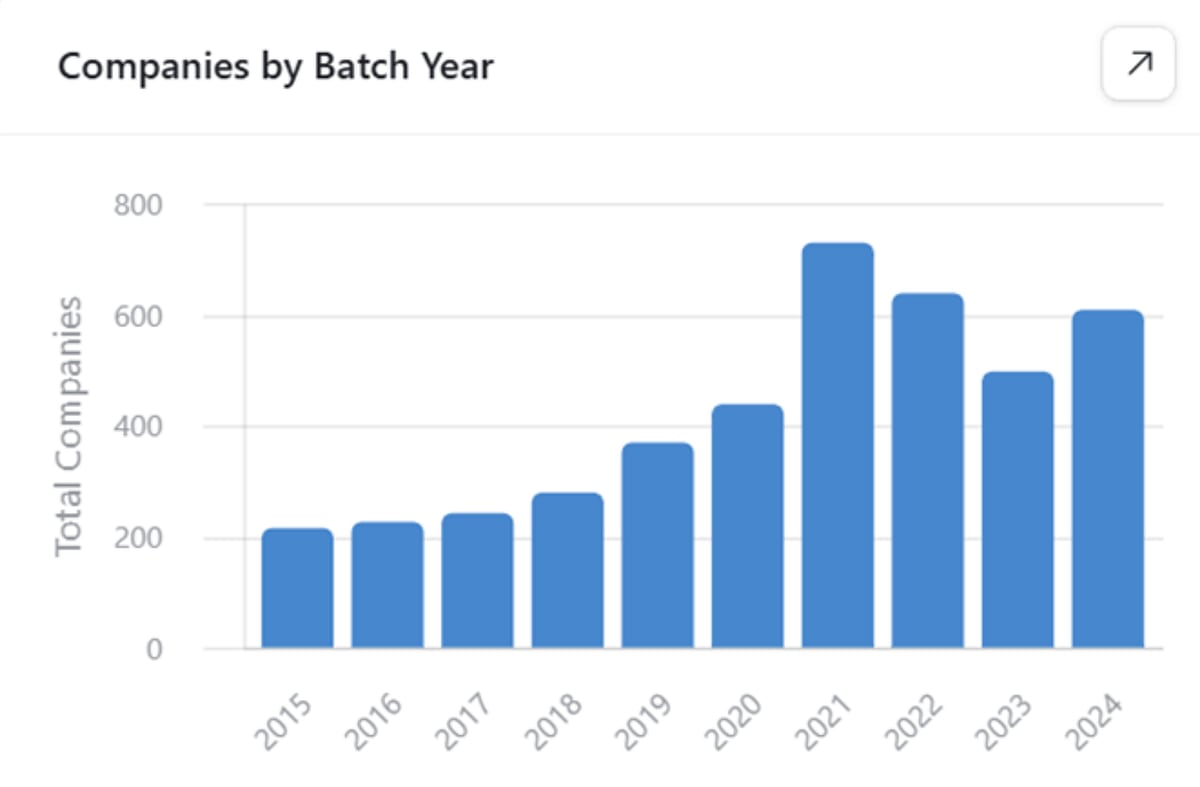

YC batches have grown 3x since 2016. I expect a significant market saturation / low hanging fruit effect, reducing the customer base of each startup compared to when there were only 200/year.

Epistemic status: I think you should interpret this as roughly something like “GenAI is not so powerful that it shows up in the most obvious way of analyzing the data, but maybe if someone did a more careful analysis which controlled for e.g. macroeconomic trends they would find that GenAI is indeed causing faster growth.”

Of the 20 companies which had the highest 2 year growth post-YC, only 1 (Tennr) was a 2023+ batch company, even though 16% of the companies I could find 2 year growth data for were 2023+.[1] The average valuation of a YCombinator company two years after it goes through YC is only $13.3M for 2023+ batches, compared to $46.1M for <2023 batches.[2]

“YC-backed” is sometimes used as a synonym for “good startup,” but the most talked-about GenAI startups (Anthropic, Cursor, etc.) aren’t YC-backed.[3] It's possible that YCombinator startups have secularly become worse, and this effect overshadows any increase from generative AI.

All code and data can be found here.

Methodology

I scraped a list of all YC-backed companies from here. I then asked Claude Haiku 3.5 (with a web search tool) to identify the valuations of each company annually after it went through YC.

Valuation numbers were adjusted using the cpi python package to be in June 2025 dollars.

I then randomly sampled results to confirm that the extracted valuations were correct. I particularly manually verified the list of the top 20 1- and 2-year growth companies.

Identifying GenAI startups

It is hard to know for sure how much a company is using GenAI. It seems safe to assume that most YC companies were not using it much before the launch of ChatGPT (if only because the technology wasn’t available), and somewhat reasonable to assume that companies were mostly using it afterward (because YC pivoted very hard into GenAI startups).

I therefore use being before or after the launch of ChatGPT as a proxy for using GenAI. This is not an ideal identification mechanism for obvious reasons but I think it’s a reasonable proxy. Importantly, Garry Tan talks about “the whole batch” growing, not “the GenAI startups in the batch”.

Sources of error

I expect there are two major sources of error in this project.

These sources of errors tend to more heavily affect the results for the average statistics and don't affect the estimates of the top companies as much. I therefore would suggest believing the top 20 lists more than the information about the average statistics.

Results

The most valuable companies 2 years after doing YC

Tennr is the only 2023+ company on this list.

The most valuable companies 1 year after doing YC

Legora is the only 2023+ company on this list.

Average Growth

The fastest growing YC batch of all time was Winter 2009. This is because it was a small batch (16 companies), one of which was Airbnb.

YC has shifted to having much larger batches (Summer 2025 was 159 companies, 10x W09). This brings down the average, and I’m not sure one should read that much into the average statistics, but I will include them for completeness.

Discussion

Garry Tan’s comments

CNBC reports:

He's repeated this point in previous interviews, e.g. saying that both Summer and Fall 2024 batches grew 10% week-on-week on average.

Tan does not say what metric he is using to measure startup growth, and the cynical reader may suspect if he was using a real metric like “revenue” he would have said so instead of leaving it unspecified. (My understanding is that YC requires companies to report some metric weekly, and this is probably what he is referring to, although it's unclear.)

If Garry or someone else from YC is reading this, I would value more insight into what exactly has been growing 10% week on week.

Has YCombinator just lost the mandate of heaven?

I do think that there is a meaningful sense in which Y Combinator startups are just not the right reference class for someone who is thinking about generative AI startups. My mental brainstorm of the most valuable GenAI startups turns up mostly companies which are not YC-backed (Anthropic, OpenAI, Cursor, Harvey, Windsurf, etc.).

My guess of the YC companies which have benefitted the most from the GenAI boom are Scale AI (S16) and Replit (W18). This seems consistent with the view that AI will make a lot of valuable companies, but they will still take 10+ years to exit.

The only two post-ChatGPT companies on the top-20 lists are both GenAI companies (Tennr and Legora). This is consistent with a view that GenAI startups are doing well and it’s just that YCombinator startups as a reference class are doing worse.

I therefore do think that these results are not as broadly applicable as they might seem. That being said, it's also hard for me to find examples of quick billion-dollar AI exits outside of YCombinator. Cursor, for example, was almost an example of a company that got acquired for billions of dollars after only two years after being founded, but didn't quite make it. So I would still generally back the claim that we have not seen many $1B+ exits <4 years after founding.[4] [5]

Stripe data disagrees, showing that AI companies are growing revenue more quickly

Stripe published this report. A key graph:

There are a couple of possible explanations for why their results disagree with my findings:

Carta’s data agrees, showing that companies aren’t growing faster

Carta’s Q2 report shows that companies are taking longer to raise initial rounds:

An optimistic interpretation of this would be that companies are able to reach profitability more quickly and therefore don’t need to raise money as aggressively. Unfortunately, if this were true I think we would see that companies valuations are increasing, but Carta actually reports a decrease in average deal size YoY:

The one exception is that average seed round size seems to have increased. My guess is that Q2 just had some outliers, but if this trend holds true in Q3 and Q4 it might indicate a real sustained shift.

Overall, this data seems consistent with the view that startups are not growing more rapidly than they used to be (although Carta’s dataset doesn’t go back very far, is fairly noisy, and is subject to various other caveats[6]).

You can still get rich quick though

While generative AI might not make it easier for people to have billion dollar companies quickly after going through Y Combinator, it also probably doesn't make it dramatically harder. My guess is that most entrepreneurs should basically assume that the results for generative AI companies are roughly in line with historical YCombinator software companies and the fact that I found them to be lower is mostly due to noise. (Whether this trend will continue is, of course, more debatable.)

The declining influence of YCombinator is maybe even a positive sign about the strength of AI: maybe AI means that you don't even need to go through YCombinator anymore and that's why the YCombinator companies aren't doing so well (the best AI companies are just successful without YC).

Further Research

If you are interested in researching this area more, I would be curious to know:

Conclusion

There are a bunch of factors which could explain the relatively sluggish performance of YC startups post-ChatGPT: high interest rates, YC being less attractive, etc. I have made no attempt to control for these and expect that, if I did, the 2023+ startups would perform better.

However, this does mean that even the most favorable interpretation of the data implies that the newer startups have their growth boosted by an amount smaller than the harm caused by factors like interest rates, which means that the benefit is relatively small.

A prediction market about whether next year will show the same results is here.

All dollar figures are in 2025 dollars, unless otherwise stated

I include averages for completeness, but think that changes in e.g. how many companies YC accepts per year make those figures hard to interpret.

Scale AI is, I think, the major exception, but they are perhaps the exception that proves the rule as they were founded in 2016 and attribute their early growth to self-driving cars.

Which is a high bar! But it is one that founders might need their company to meet if they want to exit before their labor gets substantially automated away.

I haven't measured the base rate here at all, so I don't feel very confident that this rate isn't actually higher than it was previously.

Notably their dataset covers all companies, not just GenAI ones.